UK Dairy Ingredients Market 2026: Prices, Demand, and Supplier Landscape

The UK dairy ingredients market entered 2026 under pressure from global supply tightness in butter and skimmed milk powder. This report breaks down price trends, import patterns, and what buyers should know.

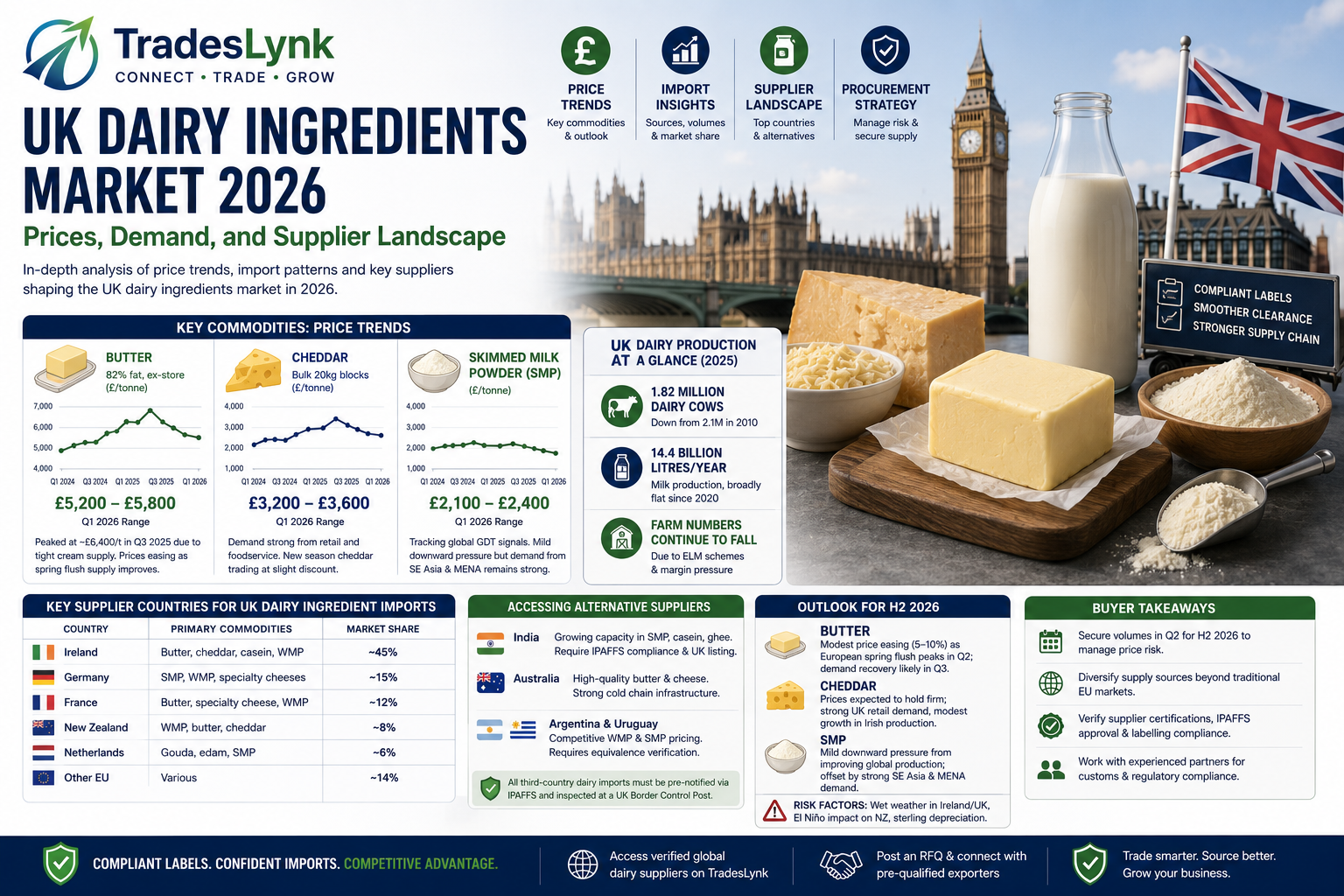

The UK dairy ingredients market entered 2026 in a state of structural tightness. A combination of declining domestic milk production, ongoing input cost pressure for UK processors, and disruptions to EU supply during 2025 pushed wholesale prices for butter, cheddar, and skimmed milk powder (SMP) significantly above their 2023 levels. For buyers — food manufacturers, retailers, and foodservice operators — understanding the market dynamics is increasingly important for managing procurement risk.

Key commodities: price trends in 2025–2026

Butter

UK wholesale butter (82% fat block, ex-store) peaked at approximately £6,400/tonne in Q3 2025 — driven by a near-simultaneous drop in European cream output and strong HoReCa recovery demand. Prices eased to the £5,200–£5,800/tonne range by Q1 2026 as Irish spring flush supply began to come through, but remain elevated by historical standards.

The butter market is particularly sensitive to the fat:protein ratio in milk: when processors favour SMP production (protein-heavy), cream supply tightens and butter prices rise. The current EU incentive structure favours SMP output, maintaining structural pressure on butter availability.

Cheddar and cheese

UK cheddar prices in Q1 2026 were in the range of £3,200–£3,600/tonne (bulk 20kg blocks) depending on specification and vintage. New-season cheddar (current year production) traded at a slight discount to mature stock. Demand remains strong from UK retail own-label and foodservice channels.

Ireland, which supplies the majority of commodity cheddar consumed in the UK, maintained strong production volumes in 2025, providing some pricing stability relative to butter.

Skimmed milk powder (SMP) and whey

SMP prices in the UK market followed global GDT (Global Dairy Trade) auction signals, trading at £2,100–£2,400/tonne through Q1 2026. Whole milk powder (WMP) remained at a premium, approximately £2,800–£3,200/tonne, driven by strong emerging market demand. Whey powder (sweet whey, food grade) was at £800–£1,050/tonne.

UK dairy production: structural decline

The UK dairy herd has been contracting for over a decade. As of 2025:

- Approximately 1.82 million dairy cows (down from 2.1 million in 2010)

- UK milk production: c. 14.4 billion litres/year, broadly flat since 2020

- Average herd size has increased (farm consolidation) but total farm numbers continue to fall under ELM (Environmental Land Management) scheme incentives and margin pressure

The implication for buyers: UK domestic supply cannot easily expand to absorb demand spikes. UK processors are increasingly reliant on imported ingredients — particularly for manufacturing-grade SMP, lactose, and permeate.

Key supplier countries for UK dairy ingredient imports

| Country | Primary commodities | Market share |

|---|---|---|

| Ireland | Butter, cheddar, casein, WMP | ~45% of UK dairy ingredient imports |

| Germany | SMP, WMP, specialty cheeses | ~15% |

| France | Butter, specialty cheese, WMP | ~12% |

| New Zealand | WMP, butter, cheddar | ~8% |

| Netherlands | Gouda, edam, SMP | ~6% |

| Other EU | Various | ~14% |

Accessing international dairy ingredient suppliers

For UK buyers looking to diversify supply beyond traditional EU sources, alternative supplier regions include:

- India: Growing dairy export capacity in SMP, casein, and ghee; requires IPAFFS compliance and UK establishment listing

- Australia: High-quality butter and cheese; strong cold chain infrastructure

- Argentina and Uruguay: Competitive WMP and SMP pricing; requires equivalence verification

All third-country dairy imports into the UK must be pre-notified via IPAFFS and inspected at a UK Border Control Post. Buyers new to importing dairy from non-EU sources should engage a customs broker with specific food and dairy experience before contracting.

Outlook for H2 2026

The consensus market view for H2 2026:

- Butter: Modest price easing (5–10%) as European spring flush supply peaks in Q2; recovery of demand likely to absorb the decline by Q3

- Cheddar: Prices expected to hold firm; UK retail demand remains strong and Irish production growth is modest

- SMP: Mild downward pressure from globally improving production; partially offset by strong demand from Southeast Asia and MENA markets

- Risk factors: Any return of wet weather in Ireland/UK in May–June; El Niño impacts on NZ production; sterling depreciation

Buyers with significant H2 2026 requirements are advised to contract volumes in Q2 where possible, or consider structured supply agreements with UK processors that include seasonal price adjustment mechanisms.

Frequently Asked Questions

Why has UK butter pricing been volatile in 2025–2026?

UK butter prices have tracked global dairy commodity volatility driven by: tight European cream supply following wet weather affecting grass yields in Ireland and Germany; strong demand from food manufacturing, bakery, and HoReCa; increased butter stockpiling behaviour by UK food manufacturers post-Brexit due to supply chain uncertainty; and the continued weakness of sterling against the euro and NZD, increasing import costs. Prices in early 2026 remain approximately 15–20% above 2023 averages on the spot market.

Which countries supply the most dairy ingredients to the UK?

The UK's largest dairy ingredient suppliers are Ireland (the dominant source for fresh dairy and butter due to geographic proximity and trade ties), Germany and France (for cheese, WMP, and SMP), New Zealand (for WMP and butter), Australia, and the Netherlands. Since Brexit, Irish dairy exports to the UK have remained the single largest supply source, representing over 45% of UK dairy ingredient imports by value.

Is there a shortage of British-grown dairy ingredients?

UK domestic dairy production is structurally declining due to farm consolidation, rising input costs, and regulatory pressures under environmental schemes (ELM). This has increased UK reliance on imported dairy ingredients, particularly for SMP, WMP, and lactose. British dairy processors (Arla UK, Müller, First Milk) export a significant proportion of cheddar while importing more flexible-format ingredients for manufacturing use.

How can international dairy suppliers access the UK market?

Post-Brexit, third-country dairy exporters to the UK must be approved under the UK's Import of Products, Animals, Food and Feed System (IPAFFS) and must have UK-listed establishment numbers. Products require a UK EXPORT Health Certificate (EHC) from the exporting country's competent authority, UK border inspection at a Border Control Post (BCP), and compliance with UK food safety standards. Suppliers from countries without UK bilateral veterinary equivalence agreements face additional testing requirements.

What is the outlook for UK dairy ingredient prices for the rest of 2026?

The consensus market outlook for H2 2026 is for butter prices to ease modestly as European output recovers seasonally (spring flush), while cheddar and SMP prices are expected to hold firm given strong global demand. UK food manufacturers are advised to lock in contract volumes for H2 2026 in Q2 where possible. Buyers seeking alternative supply from non-EU origins (e.g. India, Australia) should verify IPAFFS compliance before contracting.

Explore More Topics

More from Market Prices

Next Step

Find verified exporters and turn this research into real sourcing conversations.

Related Products

Skimmed Milk Powder UK

British Dairy Commodities Ltd · UK

Send InquiryWhey Powder Demineralised

British Dairy Commodities Ltd · UK

Send InquiryUK Casein Powder

British Dairy Commodities Ltd · UK

Send InquiryUK Butter Salted Export

Cheshire Cheese & Butter Co · UK

Send InquiryRelated Exporters

Ready to grow your export business?

Join TradesLynk and connect with verified international buyers today.

Create Free Profile